MBA Secondary 2023: Making secondary market operations efficient & risk-free

MBA Secondary 2023: Making secondary market operations efficient & risk-free

MBA Secondary Market Conference 2023 is a unique opportunity to gather insights on building efficiency, cost advantage & risk management right into your capital market trades.

MBA Secondary Market Conference 2023 is just round the corner.

Given the recent developments around mega MSR packages hitting the market, the event couldn’t have come at a better time.

This time around MBA’s core agenda hinges on digitizing capital market operations for unlocking efficiency gains - a topic that’s close to our heart.

In our experience, being able to digitize MSR transfers with automated loan boarding and asset verification has several advantages:

The entire document handling process from data verification, on both sides of sales, to MSR onboarding can be completely free from manual errors.

You not only manage to bump-up your staff productivity but also have them spend more time in decisioning & active QC.

Your overall turn-around time for capital market trades become shorter.

The quality & regulatory compliance of your collateral & loan assets improve drastically.

Needless to say, we’re super excited to attend the upcoming event between May 21-24 at New York.

We will be meeting customers, partners and advisors to share insights on how to unlock ROI on MSR transfers with selective restructuring and by deploying low effort intelligent automation.

If you are headed to MBA Secondary 2023, then let’s meet for coffee at the event & discuss more.

Now, back to our weekly round-up.

Here’s a quick peek-a-boo of what’s inside:

Mortgage job cuts to plateau soon ?

30-year FRM cools with Fed rate hike

US Home Prices Drop First Time Since 2012

Bills tabled to reverse GSE mortgage fee changes

Here’s a complete low-down 👇

Before you move on …

We would love, if you could subscribe to our newsletter.

Weekly Roundup

Mortgage job cuts to plateau soon ?

Mortgage bankers and third-party originators have been working hard to adjust their staffing levels to match current business volumes. Remember when the government stimulus in 2020 led to a massive boom, adding around 120,000 jobs?

Well, now about 80,000 of those positions have been cut, as businesses adapt to the changing market.

The big question is whether returning to 2020 staffing levels will be enough.

With financing costs going up due to measures taken to slow down inflation, it's tough to predict how much mortgage business volumes will drop.

Mike Fratantoni, a top economist at the Mortgage Bankers Association, says that a strong job market will help the housing market. But he also points out that inflationary pressures might prevent the Federal Reserve from lowering rates, which is a bit of a mixed bag for home loans.

It's interesting to note that job growth is mainly happening in health care and hospitality sectors. These growing industries help to balance out job losses in technology and the mortgage market.

According to the Bureau of Labor Statistics, the US added 253,000 jobs in April, and unemployment was super low at 3.4%. Lawrence Yun, chief economist of the National Association of Realtors, says that the tight job market is partly because around 5 million Americans have stopped looking for work since the pandemic.

Yun thinks that more jobs will be added in the coming months, increasing housing demand. If more people join the labor force, it could help ease inflationary pressure and lead to lower mortgage rates. However, the construction labor market's future might also play a big role in how much housing supply is available.

Odeta Kushi, First American Deputy Chief Economist, highlights that despite the Federal Reserve's efforts to tighten monetary policy, the construction labor market hasn't seen a major decline.

In April, residential building construction employment went up 1.3% YoY, while nonresidential grew by 3.4%. Both experienced small declines month-over-month, but it's still something to keep an eye on… Read More

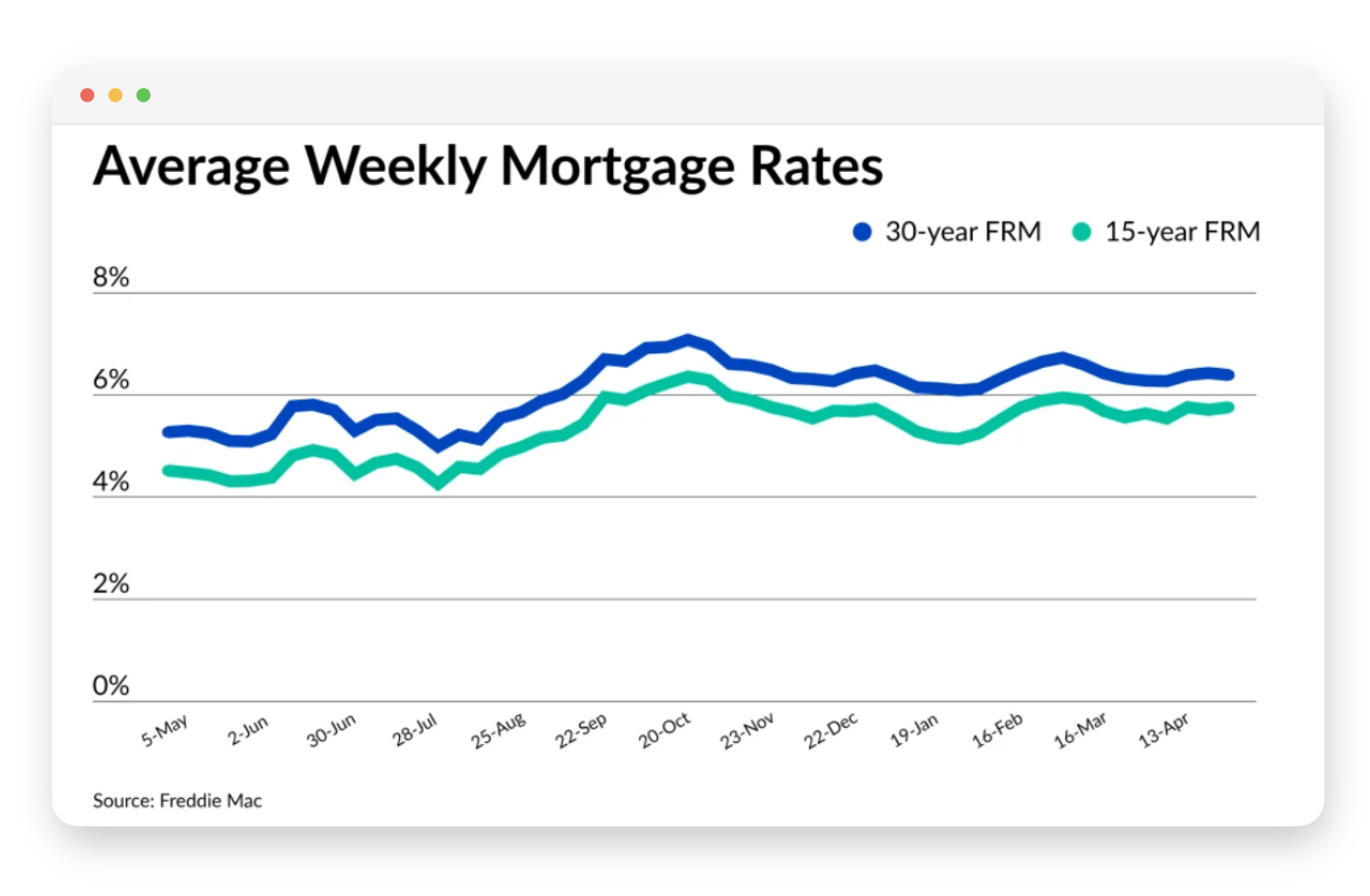

30-year FRM cools with Fed rate hike

The Federal Open Market Committee's latest 25 basis point rate hike, followed by news of a probable pause in further increases, has been positive for the housing sector.

The 30-year fixed rate loan, measured by Freddie Mac Primary Mortgage Market Survey, decreased for the first time in three weeks to 6.39%.

Sam Khater, Freddie Mac chief economist, explains that mortgage rates dropped slightly due to volatility in the banking sector and the Federal Reserve's policy outlook.

However, the lack of inventory remains a primary obstacle to affordability in the spring home purchase market. The 15-year FRM increased 5 basis points to 5.76%.

Orphe Divounguy, senior macroeconomist at Zillow Home Loans, says that the Fed will continue tightening policy until there's evidence of waning inflation, keeping mortgage rates elevated.

Mortgage rates declined after Powell's announcement due to his comments on banking sector issues. Mike Fratantoni, chief economist at the Mortgage Bankers Association, believes that this rate hike is likely the peak of the current economic tightening cycle, offering relief to homebuyers and mortgage lenders.

Zillow reported the 30-year fixed rate averaging 6.15%, down 3 basis points from Wednesday. Odeta Kushi, deputy chief economist at First American Financial, says that the potential pause in rate hikes could put downward pressure on the 10-year Treasury yield and mortgage rates.

However, if inflation data comes in hotter than expected, mortgage rates may face upward pressure for months. The Fed's signaling on a short-term pause in future hikes could be significant for mortgage originators. Fratantoni expects mortgage rates to drift down over the year as the economy slows, with the Fed lowering rates starting in 2024.

David Dworkin, president and CEO of the National Housing Conference, stresses that the affordable housing shortage in the US won't be addressed by the FOMC's potential pause.

He urges Congress to pass the Neighborhood Homes Investment Act and the Affordable Housing Credit Improvement Act. Mortgage volumes are likely to remain under pressure in 2023 due to relatively high rates… Read More

US Home Prices Drop First Time Since 2012

In February, the median sales price of previously owned U.S. homes fell for the first time since 2012, providing some relief to homebuyers dealing with high borrowing costs. The National Association of Realtors reported that the median price dropped 0.2% to $363,000, driven by a 0.7% decrease in single-family home costs. This decline coincided with a larger-than-expected increase in sales during the month.

Robert Frick, a corporate economist at the Navy Federal Credit Union, described the drop as the "strongest green shoot" in the housing market, suggesting that prices need to decline further across more markets before a general revival can happen.

Data showed that the median selling prices decreased in the West and Northeast—the nation's most expensive regions—while prices in the Midwest and South saw gains. Contract closings on existing homes increased significantly, reaching an annualized pace of 4.58 million and ending a record year-long decline.

However, the residential real estate market remains constrained by the Federal Reserve's policy tightening, which raised mortgage rates last year and discouraged many potential buyers.

The West experienced the largest annual decline in median selling prices since late 2011, dropping 5.6%. Lawrence Yun, the chief economist at NAR, believes this drop contributed to an increase in the region's sales. Median prices in the Northeast also fell 4.5%, marking the largest decrease in over a decade.

Although lower list prices may encourage more potential buyers, high borrowing costs continue to impact affordability, and the limited supply of homes for sale could restrict further price reductions.

Earlier this month, data from a Redfin Corp. report suggested that home prices may have reached their peak, as they dropped from a year ago for the first time since 2012…Read More

Bills tabled to reverse GSE mortgage fee changes

Two Republican Congress members, Rep. Andy Biggs (R-AZ) and Rep. Stephanie Bice (R-OK), have introduced bills H.R. 2928 and H.R. 2876, respectively, to cancel the Federal Housing Finance Agency's (FHFA) recent adjustments to government-sponsored enterprise (GSE) mortgage fees.

Both bills aim to roll back the GSEs' loan-level price adjustments, with over 30 Republican co-sponsors supporting Biggs' bill and 14 supporting Bice's.

Republican lawmakers have expressed concern that the new pricing leads to cross-subsidization, where borrowers with lower credit scores receive breaks at the expense of those with better payment histories. Biggs argued that the FHFA, led by a Biden-appointed director, is punishing financially responsible mortgage borrowers.

However, FHFA Director Sandra Thompson countered these criticisms, stating that cross-subsidization for lower-income borrowers, rather than those with lower credit scores, has long been part of Fannie Mae and Freddie Mac's statutory charters.

She explained that the recent changes are misunderstood, and not all borrowers with higher credit scores are penalized. Some may even see their fees decrease or remain flat due to the nuanced price changes.

Thompson highlighted that underwriting usually requires borrowers receiving a break because of their income to demonstrate other strong indicators of repayment ability. She questioned the opposition to the most recent pricing revision and said that the pricing grids needed extensive updates for modernization…Read More

And that’s a wrap. Until next time, stay healthy & keep reading.. 😊